Investing Made Easy

Let’s start with the good news.

The good news is that investing has become easier. Much easier.

It is easier because Exchange Traded Funds are now the primary investment choice for brokers, advisers, and online investment platforms.

Without realizing it, the financial adviser industry is teaching you how to invest on your own at the lowest possible cost. Using a small number of ETF’s.

I recently had lunch with my dear friend Marilyn. Marilyn manages bond portfolios for high net worth individuals.

What sets Marilyn apart from other advisers is that she buys individual bonds for her clients. She does all of her own credit research and trading. This means she is an adviser and a portfolio manager.

You are not going to find many advisers with the skill and knowledge that Marilyn has.

Individual security selection of bonds or stocks, by advisers is a lost skill.

Advisers, by their own admission, don’t pick stocks and bonds. Advisors may offer many services to clients, but investment knowledge isn’t top of the list.

The financial adviser role has shifted away from hands on investing. Other services may include estate planning, tax reporting, financial planning, or retirement advice. But those services are typically only available to very high net worth individuals.

What happens to the individual who doesn’t have millions in investable assets?

I think it is all good news for you. Using ETF’s creates a very different path for individuals to invest , for you to invest, on your own.

Exchange Traded Funds have changed the landscape of investing.

The focus of advisers is on asset allocation using ETF’s.

“Robo” advisors like Wealthfront, Betterment or Ellevest use an algorithm to determine your asset allocation .

Based on the algorithm the adviser will plunk you into ETF’s or mutual funds that “fit” your profile.

The robo advisor uses preselected ETF’s.

For example, an adviser might use 20 Vanguard ETF’s. Or 25 Blackrock ETF’s.

The reason this is good news for you, is that you can do exactly what the adviser does.

One of the online advisers openly states:

“ instead of purchasing stocks and bonds directly, we almost always invest online clients’ money in exchange-traded funds (ETFs). “

Yes, using ETF’s means that the adviser does not need to have any hands-on investment experience.

Does this surprise you?

The chart below is from the Ellevest website. [1]

What I find interesting is that they are confusing asset allocation with sector selection in the tiles below.

The actual asset classes in the tiles are:

- Equities

- Fixed Income

- Cash

- Currency

- Real Estate

The tiles represent specific sectors in each asset class.

The question to start with is: “ how much of my portfolio do I want to invest in each asset class ?”

Currencies and Real Estate are asset classes.

Emerging Markets include stocks, bonds, and currencies but Emerging Markets is not an asset class. It is a category.

Embedded in each tile is a specific level of risk. Important to know.

In this investment article we will start with a few basic interpretations.

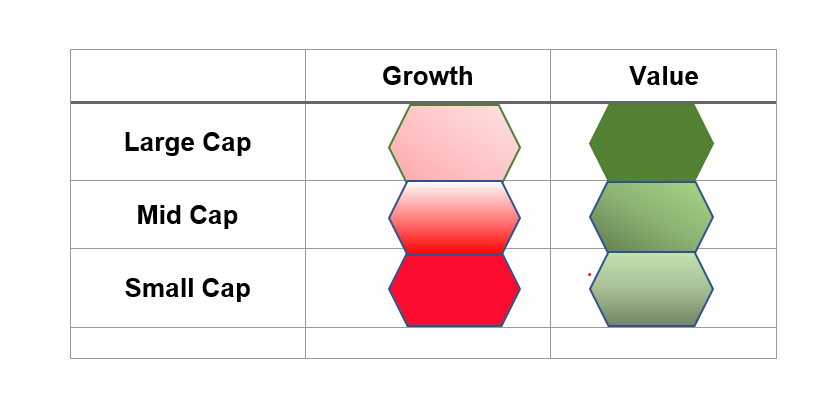

CAP means capitalization. It is the size of the company. Size is determined by the stock price and number of shares outstanding.

The reason you want to know what CAP sector you are investing in is that the size of the company is often associated with risk.

Large Cap:

The capitalization of the company is $10 billion and above. Companies in the S&P 500 ® index are large cap.

Mid Cap:

Capitalization typically ranges from $2 billion to $10 billion. The S&P MidCap 400® index is widely used to track this sector of the market.

Small Cap:

The capitalization is $2 billion and less. Companies listed in the S&P Small Cap 600® index are riskier than mid cap or large cap.

Now we toss Growth and Value into the mix.

Growth companies offer higher price potential and are inherently riskier. Growth stocks experience bigger stock price swings than Value stocks.

Growth stocks may be best suited for investors who are willing to take on more risk and who have a longer time horizon.

Value stocks provide dividend payments. Value stocks have less price volatility meaning you won’t get as much price appreciation as a growth stock (or price depreciation).

Value stocks can be safer investments than growth stocks.

Let’s rearrange the tiles the tiles on a risk basis.

In this table Small Cap Growth is the most risky and Large Cap Value is the least risky.

When you are looking for an ETF to include your portfolio you can choose an ETF based on parameters.

You can enter descriptions like “ S&P 500 Large Cap Value ETF’s” or “S&P Small Cap 600® ETF’s” in your browser

Type in : “Small Cap Growth ETF’s” and a list of ETFs’ will come up.

Or go to your brokerage website to see a list of ETFs’ that match your description.

Start with basic equity ETF’s. I will explain the other categories in upcoming investment articles.

[1] https://www.ellevest.com/magazine/investing/the-tough-standards-behind-our-etfs

This website is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, nor does it constitute an offer to provide investment advisory or other services by The Modest Economist LLC.