Investing Cash

How do I invest my cash? How much cash should I have? What should I invest in? These are questions I am frequently asked. Knowing how to invest cash poses a dilemma for most people.

This week my trading partner Lisa and I got together to discuss a few investment ideas. We vowed to make one trade that afternoon. The reason? We are both sitting on too much cash in our portfolios.

The difficulty of investing cash is that we do not know what is going to happen in the future. The future as in tomorrow or the next day or next week. Individual time horizons are going to dictate how much further in the future we are willing to go.

We are emotionally attached to the idea of having cash on hand. The notion that we need cash is deeply imbedded in our culture. “A Rainy Day” “In case of Emergency” “If I lose my job” “Remember the Depression?” “What if I invest and I can’t get my money out?” “What if the banks fail?”

What if holding cash means you are losing money? It is hard to imagine that Benny Franklin on a hundred-dollar bill will be worth less and less every year. It doesn’t matter if I put him in a bank or a drawer, holding cash has a downside.

What matters is inflation, more commonly known as prices going up. Staying in cash is not a riskless proposition. What is more likely to happen than banks failing, emergencies, a depression or rain in some parts of the country, is that inflation persists.

Over time holding cash is a drag on your purchasing power. If inflation is 2%, over the course of the year, your cash will lose 2%.

Our brains try very hard to convince us that staying in cash is a good idea. Somehow it seems “safer.” What our brain doesn’t tell us is that waiting to invest or trying to time when we invest means we are losing out.

We know that there is no certainty in the markets but there are lower risk investments for cash known as cash equivalents.

A cash equivalent can be a short-term bond, a short-term bond fund, money market funds or certificates of deposit, for example.

Note the emphasis on bonds.

Bonds and bond mutual funds are considered liquid assets. This means bonds and shares of mutual funds or exchange traded funds can be sold at any time.

This is the part where you say, “but what about penalties and fees for selling?” That is something you have to take into consideration. Depending on the interest you receive, it might be worth it to lock up some of your cash.

What we learned from our friend on the teeter totter (Bonds Part One), is that when interest rates change, the value of a bond will change, and the price of bond fund shares will change. As a bond gets closer to maturity the price becomes less sensitive to changes in interest rates. The price of a share in a short-term bond fund should also be stable.

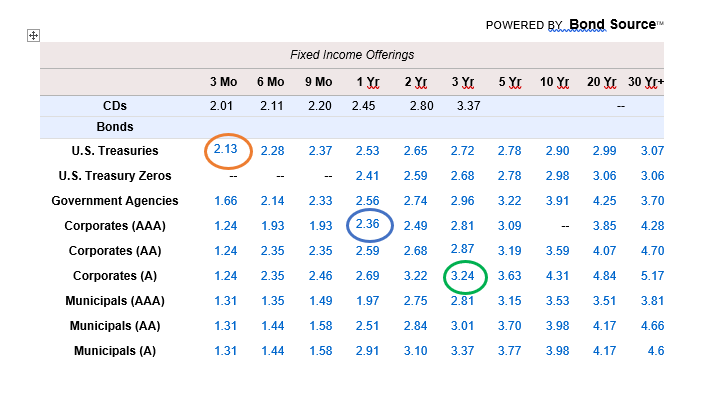

To give you a sense of where interest rates are today we can look at the following, uh, chart. Darn. It’s a chart.

The purpose of showing you a chart is to give you a point of reference. If you want to invest for 3 months, 6 months, one year or longer, you have an idea of what to expect in terms of a return.

Fixed Income Maturities and Interest Rates

Chart above is sourced from the Schwab website under Research- Bonds. The chart is called a “yield curve” and is available on many other financial sites. Data above is as of 5 September 2018.

What we are looking at is called a “yield curve.” Yield curves are the mantra of fixed income. The yield curve tells us how much different types of bonds are paying at a point in time.

Don’t get hung up on the “curve” terminology. I can show you what it looks like, but you don’t really need to know it right now.

The orange circle shows the yield or interest rate on a US Treasury Bond with a 3-month maturity. The interest rate is 2.13%. US Treasury Bonds are rated AAA by Moody’s.

The blue circle is a AAA rated Corporate Bond. It has a one-year maturity and is paying a higher interest rate of 2.36%.

The green circle is an A rated Corporate Bond. It has a three-year maturity and is paying 3.24%, higher than both the Treasury Bond and the AAA corporate bond.

As a buyer of bonds, I have a choice. Although no investment is without risk, shorter time horizons mitigate some of the risk with bonds.

One of the reasons corporate bonds pay a higher rate of interest is that they do not have the full faith and credit backing of a US Treasury bond. They also carry what is called credit risk. Credit risk refers to the company issuing the bond. So, when your brain is telling you to avoid ALL risk, your answer to your brain is that you are going to take measured risk.

Another way to mitigate risk is to spread your cash out across a timeline. I have attached a simple worksheet to help you figure out what your timeline should be.

Investing Cash Worksheet

Investing Cash WorksheetI have choices. I can buy all three maturities. The three-month Treasury bill pays 2.13% per year, a one-year corporate bond pays 2.36% a year and a corporate bond that pays 3.24% % a year. All choices are higher than the inflation rate, so my cash is going to be worth more, not less over my time horizon.

One little jargony thing you should know is that the difference in yield between the three-month Treasury Bond and the A rated corporate bond is called “the spread.” The spread in this case is 111 basis points or 1.11%.

Lisa and I spent about three hours before we managed to buy one security. We ended up buying a corporate bond. The reason it took so long is that we went back and forth, and back and forth and back and forth on our views of interest rates and the stock market. We had our own mini economic forum, discussing the reasons we thought interest rates could go up or down.

We decided on a minimum coupon of 3% and a maturity target of 5 years. Our minimum rating target was BBB-, so lower on the quality scale but we both felt confidante that the company we were looking at was not going to go belly up in the next 5 years and we were willing to take a SMALL position in our portfolios.

My rule of thumb in terms of a small position is no more than 2-3% of my total portfolio value. This is true regardless of the type of security, stocks, bonds, or funds. Minimizing the amount you buy, helps minimize your risk.

For cash equivalents I suggest looking at short term Treasury Bonds, Short Term Corporate Bond Mutual Funds, Short-Term Exchange Traded Bond Funds or CD’s.

Be sure to look any sales charges or penalties involved. If you are looking at a fund, the expense ratio is really important. Short term funds should have very low fees. By very low I would say 15 to 20 basis points.

This ended up being a much longer article than I planned, I got carried away with cash!

This website is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, nor does it constitute an offer to provide investment advisory or other services by The Modest Economist LLC.